If you’re planning to start a business with one or more partners, you’ve probably come across the term limited liability partnership. Many entrepreneurs, freelancers, professionals, and small business owners choose an LLP because it combines the operational flexibility of a partnership with the robust legal protection of a corporate entity.

But what is a limited liability partnership, how does it operate under real-world regulatory pressures, and what makes it distinct from a traditional partnership or a limited liability limited partnership business limited entity?

In this comprehensive guide, we break down the limited liability partnership meaning, analyze structural advantages, map out legal risks, and explain your compliance obligations in simple language.

What Is a Limited Liability Partnership (LLP)?

A limited liability partnership is a formal, legally recognized business structure where two or more individuals own and manage an enterprise together while enjoying distinct personal liability protections.

Core Financial Shield

An LLP avoids corporate double taxation in specific countries by utilizing pass-through taxation, where profits flow directly to individual tax returns. If the business incurs debts, experiences financial distress, or faces legal actions, the partners’ personal assets, such as personal savings, primary residences, or vehicles, are legally insulated. Under standard statutory frameworks, llp partner liability is strictly confined to the capital they have agreed to invest in the firm or as outlined in the partnership deed.

An LLP strategically bridges the gap between two legacy models:

- A traditional partnership: Retaining the decentralized management style and internal operational flexibility.

- A corporation: Gaining the coveted corporate shield of limited personal liability protection.

Because of this hybrid utility, LLPs are highly favored across global markets by licensed professionals (such as lawyers, Chartered Accountants, and architects) and fast-scaling knowledge agencies.

How Does a Limited Liability Partnership Work?

An LLP functions by establishing a clear legal boundary between the business operations and the personal finances of its partners. Unlike standard corporations, which require a rigid hierarchical separation between shareholders and a board of directors, an LLP allows its owners to manage daily operations directly.

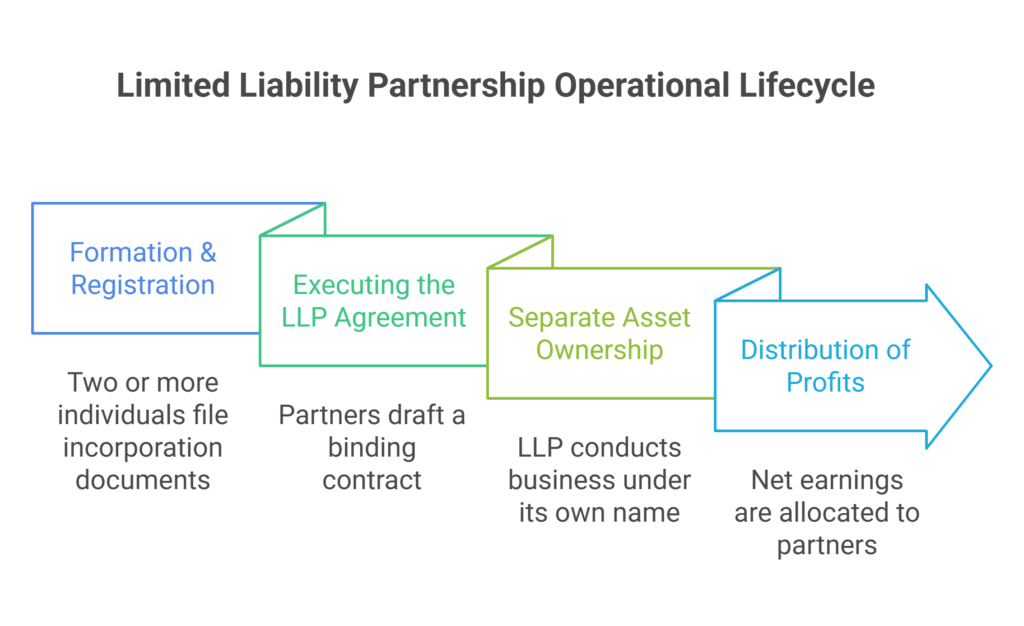

The baseline operational lifecycle follows these core stages:

- Formation & Registration: Two or more individuals file formal incorporation documents with their regional corporate registry.

- Executing the LLP Agreement: The partners draft a binding contract that dictates profit-sharing ratios, capital contribution requirements, decision-making protocols, and asset distribution terms upon dissolution.

- Separate Asset Ownership: The LLP conducts business, holds liabilities, opens commercial bank accounts, and signs contracts under its own registered name.

- Distribution of Profits: Net earnings are allocated directly to the partners according to the pre-agreed terms outlined in the governing agreement.

Key Features of a Limited Liability Partnership

1. Limited Personal Liability

The cornerstone of this model is the clear definition of llp partner liability. Partners are insulated against business debts, unfulfilled commercial loans, and organizational lawsuits. Your liability is strictly capped at your committed capital contribution, protecting your private wealth from corporate insolvency.

2. Separate Legal Identity

An LLP possesses its own legal identity independent of the individuals who comprise it. This means the entity itself can buy, sell, or hold real estate, enter into legally binding contracts, employ staff, and initiate or defend lawsuits in a court of law.

3. Flexible Management

Unlike traditional corporations that are bound by rigid governance rules, such as mandatory board meetings, independent directors, and strict shareholder voting blocks, LLP structures allow partners to design customized management frameworks directly within their partnership agreement.

4. Custom Ownership Structure

Ownership and compensation structures are highly customizable. Partners can freely negotiate disproportionate profit-sharing ratios that do not match capital contributions, tiered voting rights based on senior operational roles, and customized equity vesting schedules for founding members.

5. Perpetual Succession

The continuity of an LLP is unaffected by the retirement, insolvency, insanity, or sudden demise of a partner. The entity continues its legal existence seamlessly, provided the minimum statutory requirement of two partners is maintained or restored within local regulatory timelines.

Advantages vs. Disadvantages of an LLP

To evaluate if this business model fits your long-term growth plan, it is essential to look at a balanced overview of its benefits and practical limitations.

Advantages

- Shielding Private Wealth: Eliminates the catastrophic risk of losing personal assets due to unforeseen commercial bankruptcies.

- Operational Simplicity: Avoids the extensive administrative overhead, proxy voting mandates, and corporate secretarial complexities typical of public or private limited companies.

- Avoidance of Corporate Double Taxation: In several major jurisdictions, including the United States and the United Kingdom, LLPs enjoy pass-through tax treatment. The entity itself pays no direct corporate income tax; instead, profits pass directly to the partners, who report it on their individual tax returns.

- Enhanced Brand Credibility: Operating as a registered LLP projects a higher level of institutional stability and compliance to clients, banks, and vendors compared to an unregistered sole proprietorship.

Disadvantages

- Restricted Capital Scaling: Because an LLP cannot issue public shares or create distinct classes of equity, it is often fundamentally unsuited for high-growth startups seeking venture capital or institutional private equity funding.

- Public Financial Disclosure: In regions like the UK and India, LLPs are legally mandated to file annual financial accounts and statements of solvency with public registries, removing absolute financial privacy.

- Jurisdictional Regulatory Shifts: Tax advantages and liability rules are highly localized. For example, while the US treats LLPs as pass-through entities, India applies a flat corporate tax rate to LLPs, completely eliminating the pass-through tax benefit.

- Minimum Member Threshold: A single entrepreneur cannot run an LLP long-term; it requires a minimum of two partners to remain legally compliant.

Cross-Border Tax & International Compliance Considerations

Operating a multinational limited liability partnership introduces complex tax obligations that cross-border entities must navigate. When an LLP acts as a dual-resident entity or has corporate partners spanning major cross-border commercial links, such as the United States, the United Kingdom, or India, the domestic pass-through tax treatment can cause intense regulatory friction.

The core issue lies in asymmetric entity classification. While the Internal Revenue Service (IRS) in the United States and Her Majesty’s Revenue and Customs (HMRC) in the United Kingdom primarily view an LLP as a transparent pass-through vehicle, other statutory frameworks, such as the Ministry of Corporate Affairs and the Income Tax Act in India, treat the LLP as an opaque corporate body subject to flat corporate tax rates. This asymmetry can trigger unexpected permanent establishment (PE) risks for foreign partners. If a partner based in London or New York manages an enterprise that performs service delivery within another territory, local tax authorities may assert that the foreign partner constitutes a fixed place of business. This exposure subjects the corporate partnership to complex local filing regimes, local withholding taxes on cross-border profit distributions, and stringent transfer pricing audits.

To mitigate these legal exposures under Double Tax Avoidance Agreements (DTAA), international firms must clearly isolate trade activities from passive investment roles within their private partnership agreements. Furthermore, multi-state or multi-country operations necessitate strict transactional modeling. All cross-border fees, management overhead recharges, and intellectual property licensing agreements between localized branches must reflect arm’s length terms to survive intensive regulatory audits by global fiscal authorities.

Also Read: Furlough Meaning

Comparative Analysis: LLP vs. Alternative Structures

Table 1: Limited Liability Partnership vs. Traditional Partnership

| Feature | Traditional Partnership | Limited Liability Partnership (LLP) |

| Personal Liability Exposure | Unlimited (Joint and Several Liability) | Strictly Limited to Agreed Capital Contribution |

| Legal Status of Entity | Not recognized as a separate legal persona | Legally independent distinct corporate entity |

| Asset Protection Shield | None; personal assets can be seized for business debts | Complete protection of personal assets from business debts |

| Governance Document | Partnership Deed | Formal Registered LLP Agreement |

| Statutory Registration | Optional in many regions | Mandatory legal requirement prior to trading |

Table 2: Limited Liability Partnership vs. Limited Liability Company (LLC)

| Feature | Limited Liability Partnership (LLP) | Limited Liability Company (LLC) |

| Primary Target Audience | Regulated professional service firms and multi-partner firms. | General commercial businesses, single founders, and e-commerce brands. |

| Management Architecture | Directly managed by the equity partners. | Can select either member-managed or external manager-managed options. |

| Liability Protections | Protects partners from business debts and the malpractice of co-partners. | Protects all members broadly from general entity debts. |

| Operational Flexibility | High internal flexibility governed via the LLP agreement. | High flexibility governed via the LLC operating agreement. |

| Filing & Transparency | High public transparency required. Mandated annual financial account filings open to public registries in regions like the UK and India. | Variable public exposure. Most jurisdictions do not require public disclosure of private internal operating agreements or financial health statements. |

Strategic Guide to Forming an LLP

Phase 1: Jurisdictional Registration

Secure Name & Appoint Designated Members. First, secure a completely original business name that includes the mandatory legal suffix “LLP”. Simultaneously, identify at least two legal partners and designate who will bear the statutory responsibility for administrative compliance.

Phase 2: Structural Capital Allocations

Draft the LLP Agreement & Incorporate. Next, draft a customized LLP agreement outlining capital input thresholds and profit divisions. File formal incorporation forms with your regional regulatory authority (e.g., Secretary of State or Ministry of Corporate Affairs) along with the requisite filing fees.

Phase 3: Statutory Licensing

Obtain Tax IDs and Corporate Bank Accounts. Finally, secure your corporate tax identification numbers and any mandatory industry permits. Establish separate, dedicated commercial banking accounts to prevent any commingling of personal and corporate capital, which could otherwise compromise the integrity of your limited liability status.

Deep Dive: Managing Partner Liability in an LLP

What Exactly is the Liability of an LLP Partner?

A partner’s financial exposure is fundamentally restricted to their explicit financial commitment to the firm, alongside any explicit personal guarantees signed to secure corporate bank loans. A partner is completely shielded from general business debts that exceed the financial reserves of the LLP and operational breach of contract claims driven by other teams within the firm.

Can One Partner Be Held Responsible for Another Partner’s Mistakes?

Statutorily, the answer is no. Consider this corporate risk scenario: If Partner A commits severe professional malpractice or acts negligently during a client engagement, the client can sue the asset base of the LLP itself and target the personal assets of Partner A. However, the personal assets of Partner B remain legally protected, provided Partner B was not directly supervising the project, was not personally involved in the negligent action, and had no knowledge of the misconduct.

Conversely, if Partner B signs an explicit personal guarantee to secure a commercial bank loan for the firm, or directly orchestrates fraudulent trading alongside Partner A, the statutory corporate liability shield is pierced. In those specific scenarios, joint and several liability returns, rendering both individuals personally liable for the ensuing corporate debts.

Frequently Asked Questions (FAQs)

A limited liability partnership is a hybrid corporate business vehicle that allows two or more partners to manage an enterprise collectively while providing each individual partner with a robust shield against personal liability for the firm’s debts and obligations. Unlike general partnerships, it establishes an autonomous corporate entity that isolates corporate risks from private personal holdings.

Statutorily, a limited liability partnership definition states it is a corporate body and a distinct legal entity separate from its partners. It features perpetual succession, possesses its own capacity to enter into binding contracts, and requires formal registration and regulatory compliance updates with regional government corporate regulatory authorities.

The liability of an LLP partner is restricted to their stated capital investment in the firm, protecting their personal wealth from the organization’s debts or the professional malpractice of fellow partners. This core layer of llp partner liability insulation keeps their personal savings, primary residences, and private wealth safe from commercial bankruptcy or co-partner omissions.

No. Unlike traditional corporate entities, an LLP cannot issue public shares or raise capital through public stock exchanges, which makes it less suited for firms looking to scale rapidly via venture capital. Capital generation is structurally restricted to equity contributions from active partners or specialized banking loans.